Carry Trading Explained

by Andrew McGuinness Jul 16, 2019

History of carry trading

Until the 1990s, large hedge funds made a fortune betting on emerging-market currencies. At the time, the term carry trade was little known to most of the financial world. But then Bank of Japan, in their battle against deflation, decided to cut interest rates and employ a zero interest-rate policy (ZIRP). Many traders worldwide saw the opportunity in large interest rate differentials between the economies in countries like the low-interest-rate Japan on one side, and Australia and the U.S. on the other, where the latter had an interest rate at around 5%. At this time, carry trading was mostly done by investors in government bonds and other fixed-income assets.

Twenty years later, the Federal Reserve lowered the fed funds rate to near zero and that caused the yen carry trade with the dollar to take a brief pause. However, the yen was still borrowed to purchase higher-yielding currencies such as the Australian dollar, the Turkish Lira, and the Brazilian real. At the time, the Australian dollar had a 4.5% return.

In late 2012, the yen trading picked up when the Japanese Prime Minister Shinzo Abe promised to boost economic growth, lower interest rates, and open up trade. In the first three years of this decade, the yen carry trade rose by 70%. However, in 2013 the Japanese economy went back into recession. The Bank of Japan made another round of quantitative easing, which caused the yen to fall to a seven-year low in 2014. Even today, the Bank of Japan struggles to keep the yen low, despite its low interest rate and quantitative easing measures. During this time, not everyone succeeded in carry. In 2013 a U.S. hedge fund that managed more than $14 billion went bust as interest rates across the developed world dropped to zero. As addition to that, many central banks in their effort to boost growth implicitly tried to weaken their currency, which made it hard to determine long-term trends.

In 2016 the Bank of Japan introduced a negative interest rate. This means that a depositor is charged a percentage of their money if they keep it in an account. The logic here is to punish banks that hoard cash instead of giving loans to businesses. With an interest rate of -0.10% the central bank will charge commercial banks 0.10% on some of their deposits. In theory, this is supposed to encourage commercial banks to lend money, which in turn would boost domestic spending and business investment.

Japanese yen remains the favorite for carry trades even today in 2017. The Bank of Japan continues to keep interest rates low while other countries have taken a more hawkish stance on the matter.

What is this interest rate?

When a central bank lends funds to a commercial bank, the charges paid on those funds are called bank rates or interest rates. This is one of the more effective tools in the central banks’ arsenal in their monetary policy. Changes in interest rate control money supply in the economy and the banking sector, it controls inflation, and stabilizes the country’s exchange rate. Whenever an interest rate is changed, it causes a ripple effect in the stock market, the currency exchange market, and the country’s economy. And that is what large investors and hedge funds keep an eye on.

What is carry trading?

Carry trading is a strategy in which an investor borrows a certain currency with a low interest rate to finance the purchase of a different currency or an asset (usually government bonds) with a higher interest rate, and carry it until it makes a profit. Depending on the amount of leverage used, the difference between rates can be substantial.

In the forex market, carry trade is simply taking a long position in a high-interest rate currency and at the same time taking a short position in a low-interest rate currency. Upon settlement, the trader receives the difference between the forward rate and the spot rate. This is also known as a forex swap.

How does carry trading work?

According to economic theory, an investment strategy based on exploiting differences in interest rates across countries should yield no predictable profits - i.e. it shouldn’t work. After all, if a country has a high interest rate, something is wrong; it either has poor economic fundamentals or high inflation. But in reality, investors are prepared to overlook fundamentals for a decent profit. These investors help strengthen high-interest-rate currency by increasing demand. As more traders get involved, the price of the currency can soar and harm the country’s economy. When that happens, central banks can intervene and lower interest rates, thus lowering demand for their currency. And when that happens, usually carry trade unwinding comes next.

So how do traders carry?

For our example let us say that the Japanese yen has an interest rate close to 0%, while the U.S. dollar has 1.25%. In this case, the trader is expected to profit 1.25%, which is the difference between the two interest rates. The process of carry trade strategy goes as follows:

- First, the trader has to borrow yen and convert it into dollars. With the current rate of 112.5 yen per dollar, the trader borrows 10 million yen and purchases $88,888 (10,000,000/112.5 = $88,888).

- With the dollars, the trader buys securities that pay the U.S. rate (government bonds, for example). After a year of holding the position, the trader has $1,111 ($88,888 x 1.25%)= $1,111).

- Now, the trader has to return the 10 million yen. Presuming the exchange rate remained the same during the year, the trader has made 1.25%; However, if the yen weakened, the profit would have been higher and vice versa - if the yen got stronger the trader would have earned less or even suffer losses when he would sell the dollars to buy yen.

All this was achieved with 1:1 leverage. But in a market where leverage can be up to 500:1, the returns can be quite enticing.

Why some countries have high interest rates and some low?

In a research paper called Commodity Trade and the Carry Trade: A Tale of Two Countries the authors Robert Ready, Nikolai Roussanov, and Colin Ward, they examine the phenomenon of commodity-exporting countries (like Australia and New Zealand) that have high interest rates, compared to importers of basic goods (like Japan and Switzerland) that export expensive manufactured goods. According to the paper, the money managers who do both commodity and currency carry trades are taking high risk, especially because of currency fluctuations and correlation between commodities and currencies. However, on average, fluctuations rarely wash out the difference in interest rates.

In the last thirty years, a typical carry trade strategy involves Australian dollar and New Zealand dollar as they have historically high interest rates, and Japanese yen and Swiss franc with low interest rates. These countries have different structure of their production and international trade. Japan and Switzerland import basic commodities and turn them into high-tech, high-quality manufactured goods that they export, while Australia and New Zealand primarily export basic commodities like iron ore or natural gas. The main question in the research paper is: does the difference in fundamentals of the countries’ economies explain the difference in their interest rates historically? This interest rate differential is known as risk premium.

The currencies of the commodity exporter countries are known as commodity currencies and their exchange rate goes up or down when commodity prices go up or down accordingly.

The authors of this paper claim that there is a reason to think that the commodity currencies bear higher risk to investors in the financial markets, than currencies of exporters of manufactured goods like Japan and Switzerland, which are in turn called safe haven currencies.

In the global economy, commodity prices go up in times of global expansion, and they fall during economic crisis. This is one of the reasons that these currencies are considered risky. On the other hand, the currencies of sophisticated manufactured goods exporters like Japan and Switzerland, appreciate in downturns, basically acting like a hedge against the global economic conditions.

How does carry trading affect the global economy?

Today, the currencies from countries like Japan, the U.S., or even the EU, are borrowed and invested in the big emerging markets where their currencies have the highest-yielding interest rates. For example, Russia has an interest rate of 8.25%, Brazil 7.50%, and India 6.00%. Those are all enticingly good options to invest in. However, when a debt reaches a certain point and the country has trouble paying the interest on its debt, there is a huge unwinding of positions. Hundreds of millions of dollars leave the country, producing a market crisis and possibly a world-wide market crash. The emerging markets carry trade is estimated to be trillions of dollars in size. But unlike emerging economies, the larger economies in the developed world, like Japan and the U.S., have certain immunity to the disruptive nature of carry trade due to the massive quantity of their currencies.

Central Bank | Interest Rate | |

Swiss National Bank (SNB) | -0.75% | |

Bank of Japan (BOJ) | -0.10% | |

European Central Bank (ECB) | 0.00% | |

Bank of England (BOE) | 0.50% | |

Bank of Canada (BOC) | 1.00% | |

Federal Reserve (FED) | 1.25% | |

1.50% | ||

Reserve Bank of New Zealand (RBNZ) | 1.75% | |

People's Bank of China (PBOC) | 4.35% | |

Reserve Bank of India (RBI) | 6.00% | |

Central Bank of Brazil (BCB) | 7.50% | |

8.25% |

When does carry trading work best?

- Since carry trade is mostly affected by interest rates, the best environment to profit is when central banks increase interest rates or intend to increase them. In this case, the attractiveness is not only in the passive interest yield, but in the currency appreciation.

- When a central bank increases the interest rate, small traders, large investors, and hedge funds tend to notice and move their capital in that particular currency, driving its value up by increasing demand.

- In conditions of low volatility carry trades tend to perform well, because currency fluctuation won’t offset gains.

When does carry trading fail?

- If central banks decrease interest rates or plan to decrease them it will cause traders and investors to sell the currency and move their capital to a higher-yielding currency or asset.

- For countries that are export oriented (like Australia or New Zealand), an excessively strong currency could force the central banks to react and stem the rise. When a central bank intervenes in the currency, either to stop it from appreciating or depreciating, it could impact the gains in carry trade.

- When positioning gets crowded and correlated, unwinding may come next.

What is the best way to profit from carry trading?

>span class="s7">long-term strategy. This makes it suitable for investors rather than day traders, as they do not have to watch price quotes every hour of the day. Once the carry trade is executed, the investor has to wait until his position becomes profitable.

Are the returns worth it?

According to the Bloomberg Cumulative FX Carry Trade Index, which tracks performance of eight-emerging market currencies against the U.S. dollar, carry trading has had a positive return in 11 out of 17 years, and usually outperforms stocks. Of course, if you add the high leverage mentioned earlier, the returns can be impressive.

How big is the global carry trading and how does it affect currency exchange rates?

Evidence of the international financial transactions and investment positions associated with carry trade are limited, mostly because these strategies are conducted through transactions known as currency swaps which are hard to monitor. However, two studies from the Bank of International Settlements, shed some light on the size of carry trade activity and their effect on exchange rate movements. One of those studies show that between 2001 and 2004 there was an increase in turnover due to carry trade activities on Australian and New Zealand dollars, which at the time had high interest rates. The carry trade pushed these two currencies higher versus the lower-yielding U.S. dollar and the Japanese yen. This study also found that between 1992 and 2004 the forex market turnover was strongly related to interest rate differentials.

The second study concerns the cross-border claims denominated in yen, which showed substantial growth in 2005. This showed that yen was the primary currency used for carry trade.

Carry trading in forex

In the forex market, currencies are traded in pairs (if a trader buys EUR/USD, they buy EUR and sell USD at the same time). This means that a trader collects interest on the currency they buy (EUR in our case) and pays interest on the currency they sell (USD in our case). Unlike government bonds and other fixed assets, in forex, interest is paid at end of the day. Basically, forex brokers debit/credit the trader overnight (when the New York session ends at 22:00 GMT). This carrying in forex is called rollover.

Thanks to high leverage, carry trade is a popular strategy on the spot forex market.

In a hypothetical trade AUD/JPY buy and hold position with the size of one standard lot, if it were opened in 2004 and closed ten years later it would have looked like this:

Year | Net Interest | Income | Exchange P/L | Total P/L |

2005 | 4.70% | $4,714 | -$420 | $4,294 |

2006 | 4.90% | $9,567 | $6,040 | $15,607 |

2007 | 5.30% | $14,842 | $13,680 | $28,522 |

2008 | 4.00% | $18,845 | $17,370 | $36,215 |

2009 | 3.40% | $22,271 | -$17,100 | $5,171 |

2010 | 3.10% | $25,392 | $3,020 | $28,412 |

2011 | 4.20% | $29,608 | $2,345 | $31,953 |

2012 | 3.80% | $33,452 | -$1,764 | $31,688 |

2013 | 2.40% | $35,831 | $9,512 | $45,343 |

2014 | 2.20% | $38,013 | $12,941 | $50,954 |

Totals | 3.80% | $38,013 | $12,941 | $50,954 |

The interest rate income was $38,013, while the exchange rate gain was $12,941. It basically made a 19.8% annual return in this ten-year period.

How to recognize good carry trading opportunities?

When the outlook of a country’s economy is good, the chances are that their central bank will raise interest rates to combat inflation. Higher interest rate will attract investors who seek high-interest rate bonds, and this in turn will increase demand for its currency, thus boosting its value and creating further profit potential. However, due to high leverage in forex, the long-term view on the currency pair has to be favorable if a trader is to buy and hold.

How to avoid bad carry trading opportunities?

When the country’s economy outlook is grim, central banks may lower interest rates to depreciate their currency to fight deflation and make their exports cheaper and more competitive abroad. The low interest rates will make carry-trade investors sell the currency, thus further lower its value, and seek better investment opportunities elsewhere.

Carry trading and risk

In forex, carry trade works best when there is low risk aversion. This means that traders and investors often buy commodity currencies (like Australian and New Zealand dollars) and sell safe haven currencies (like Japanese yen and Swiss franc), but when the risk aversion is high, the aforementioned traders tend to move their capital to the low-yielding safe haven currencies.

Another type of risk that a trader has to be aware of is the exchange rate risk. This means that a currency’s price can fluctuate and offset carry trade gains; it can even cause losses. That is why some traders use hedging strategy to limit exposure.

Selecting a pair for carry trading

To find the best pair to carry, a trader has to look for high interest rate differential. Today, from the major currency pairs, New Zealand dollar has 1.75% interest rate and Swiss franc has -0.75%.

Next comes to look for a stable uptrend in favor of the higher-yielding currency, in our case buy NZD/CHF. This will not only give profit off of the interest rate differential, but from the currency appreciation as well. Unfortunately, NZD/CHF pair doesn’t fulfill the second condition, so we move to the next suitable pair.

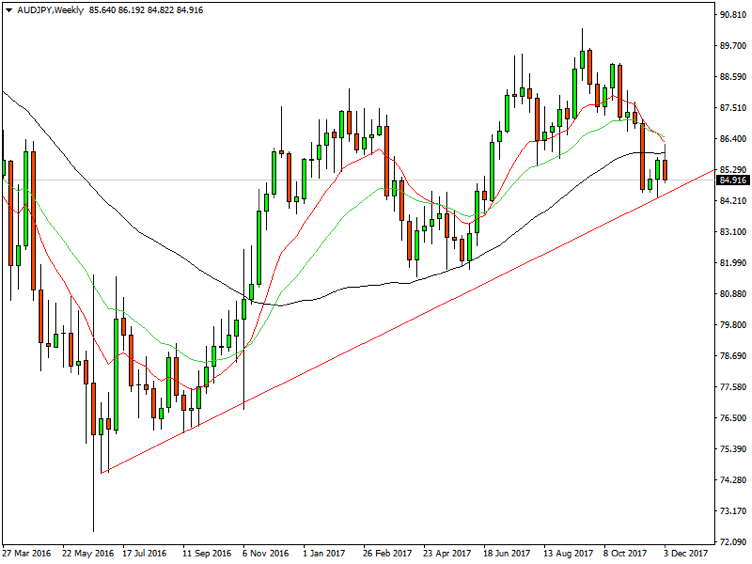

Today, AUD/JPY is still the best pair to carry. Australian dollar has interest rate of 1.50% while Japanese yen has -0,10%. And looking at the chart below, we can see that the pair has been in a steady uptrend since June 2016.

Does carry trading work on every forex broker?

Unfortunately, no. Not every forex broker offers the same rollover conditions. Charges can vary across currencies as well, which can make this strategy unprofitable. So before deciding to use carry trade strategy on any pair, find a broker that has the best rollover conditions. These are usually listed on the broker’s trading platform.

Money management

With the possibility to use high leverage in forex, the possibility to lose a large part of the trader’s account is equally high. That is where money management comes in. First, a trader has to determine their risk tolerance.

Most commonly used risk per trade is 2%, though a more aggressive trader would prefer 5%. Of course, this is not a rule carved in stone, but merely a guideline.

But before deciding on the size of risk to use, keep in mind the following:

Amount of equity lost | Amount of return necessary to restore to original equity value |

25% | 33% |

50% | 100% |

75% | 400% |

90% | 1,000% |

This should put the importance of money management into perspective.

Conclusion

Carry trading is a popular strategy not only for hedge funds and large investors, but for small traders as well. Despite the pessimistic observation from the economic theory that carry trade shouldn’t work, we’ve seen multiple times in financial history that when managed correctly it can be profitable.

Things to keep in mind:

- Observe interest rates. More often than not, they are the main driver of currency exchange rate.

- Determine long-term currency direction. Since carrying is a long-term strategy, having a clear overview of the price movement is necessary.

- Money management. If a certain currency pair has a good carry trade opportunity, determine risk tolerance before entering a trade.

- Take profit or cut losses. As soon as interest rates change, or there is a shift in central bank policy, close the position and wait for a better opportunity.